Two dominant perspectives often frame the debate about linking property taxes to public services. The “wealth tax” perspective suggests that those who own more expensive properties should pay a higher tax rate than those with basic properties, with the revenue being redistributed to benefit the broader community.

Conversely, the “benefit tax” viewpoint argues that those who pay higher property taxes should receive public services proportional to their contributions. In practice, most property tax systems incorporate elements of both perspectives, often implicitly.

The relationship between residents of the Karen Langata District Association (KLDA) and the City of Nairobi illustrates these contrasting perspectives on property tax purposes.

Founded in 1940, the KLDA represents the interests of Karen and Langata residents in Nairobi, ensuring well-serviced road infrastructure, street lighting, and security in the area. Most KLDA members are professionals and wealthy landowners who have collectively organized to advocate for better services.

Property Tax as a “Benefit Tax”

In 1995, the KLDA became the first association in Kenya to take legal action against the City of Nairobi, demanding greater transparency and improved service provision. A court decision granted KLDA the right to withhold property taxes and direct these funds into a special account managed by the Association. The revenue collected would then be transferred to the City of Nairobi, provided the City delivers a development plan endorsed by KLDA members before implementation.

This ruling established a system where property tax was explicitly understood as a benefit tax paid in exchange for public service investments like road or waste collection in the Karen Langata community.

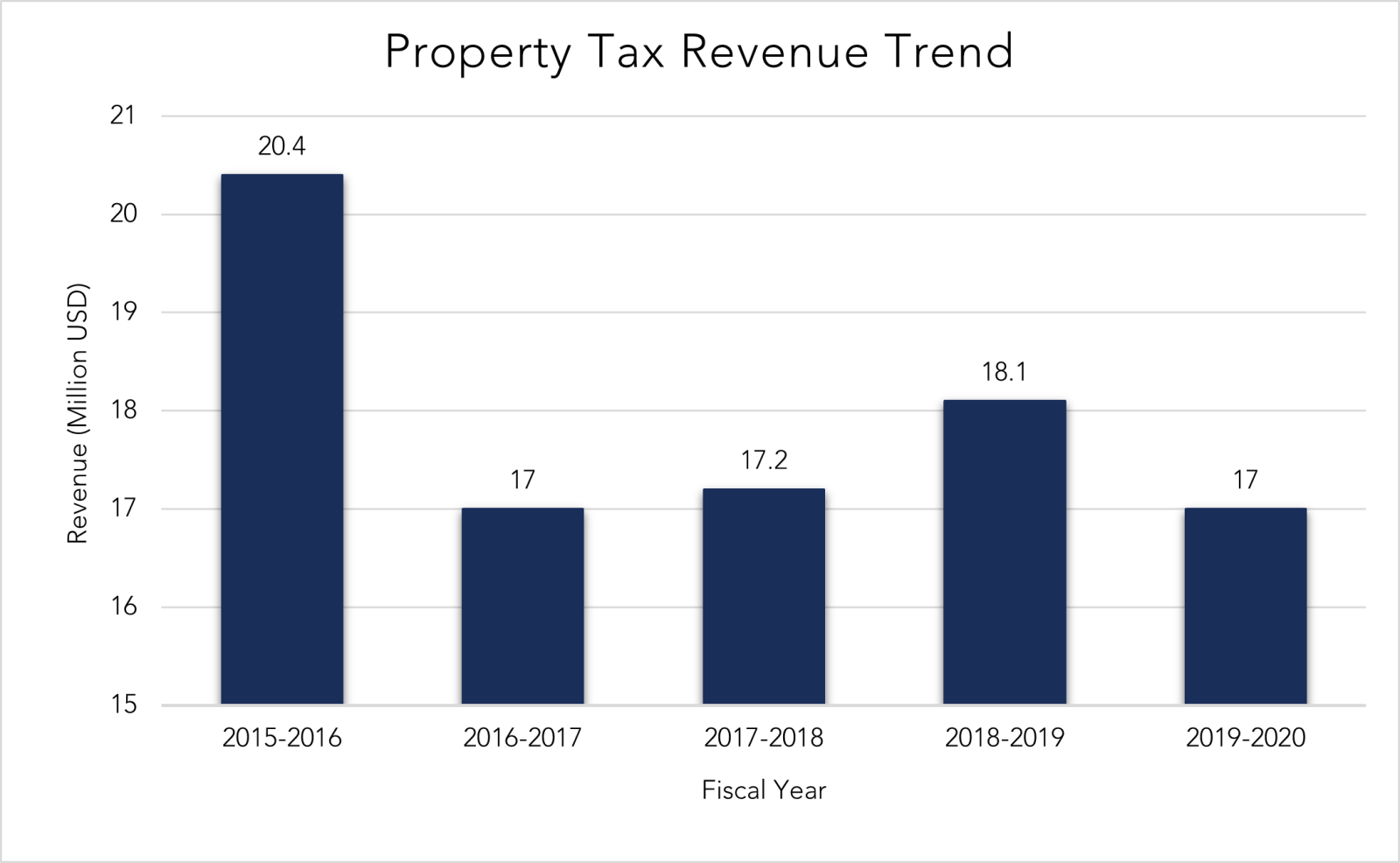

During fieldwork in Nairobi in March 2018, KLDA members indicated that they collect between US $147,000 and US $167,000 in property tax revenues annually (15-17 million Kenya Shillings).

While this represents only 0.7 percent of property taxes in Nairobi, it constitutes a significant share of residential property tax collection.

Property Tax as a “Wealth Tax”

While the KLDA views property tax as a benefit tax, Nairobi City officials regard it as a wealth tax. According to them, property tax revenues should finance overall community services, not just those in the neighbourhoods that pay the tax. They viewed the KLDA’s actions to withhold property taxes and demand services in exchange for payments as unlawful. Former Governor Evans Kidero expressed his opinion that it was “morally wrong” for residents to avoid paying rates, placing a heavier burden on residents in other neighbourhoods.

The issue was particularly controversial because Karen and Langata are among the wealthiest parts of Nairobi. They were historically populated by Europeans during the colonial period and remained home to a significant European population post-independence. Consequently, the KLDA’s insistence on controlling the use of their property tax payments took on both class and racial dimensions.

In 2015, Governor Kidero took the KLDA to court to compel its members to pay property taxes directly to the City. Nairobi won the case, but the KLDA continued to demand more accountability from the City. These efforts led to the 2017 Recognition Agreement, allowing KLDA members to sign off on any new development projects before implementation. Through this agreement, KLDA maintained a strong voice in shaping development in their area. However, in practice, implementation of the agreement has been mixed, with members often finding their efforts to engage City officials relatively unsuccessful.

Accountability and Equity in Property Taxation

The relationship between the KLDA and Nairobi City highlights a central conceptual and political tension when trying to strengthen property taxes and service delivery.

On the one hand, the KLDA’s persistent efforts to control property tax revenues and the projects they fund aimed to ensure greater accountability in the use of public funds. Withholding property tax revenues until mutual agreement of service delivery plans amounted to an extreme form of earmarking property tax revenues for service delivery.

On the other hand, this arrangement raised concerns that the push for accountability was also an attempt, intentional or not, by wealthy property owners to opt out of general taxation and demand public services of higher quality than those available to the general public. Viewing property taxes as a benefit tax can be used by wealthier and more influential taxpayers to avoid contributing to the public good. There is a distinction between seeing property taxes as a means to provide local benefits and arguing that property taxes should only benefit the neighbourhoods that pay. The former creates pressure for accountability in revenue use, while the latter seeks to entrench inequalities in service quality between rich and poor neighbourhoods.

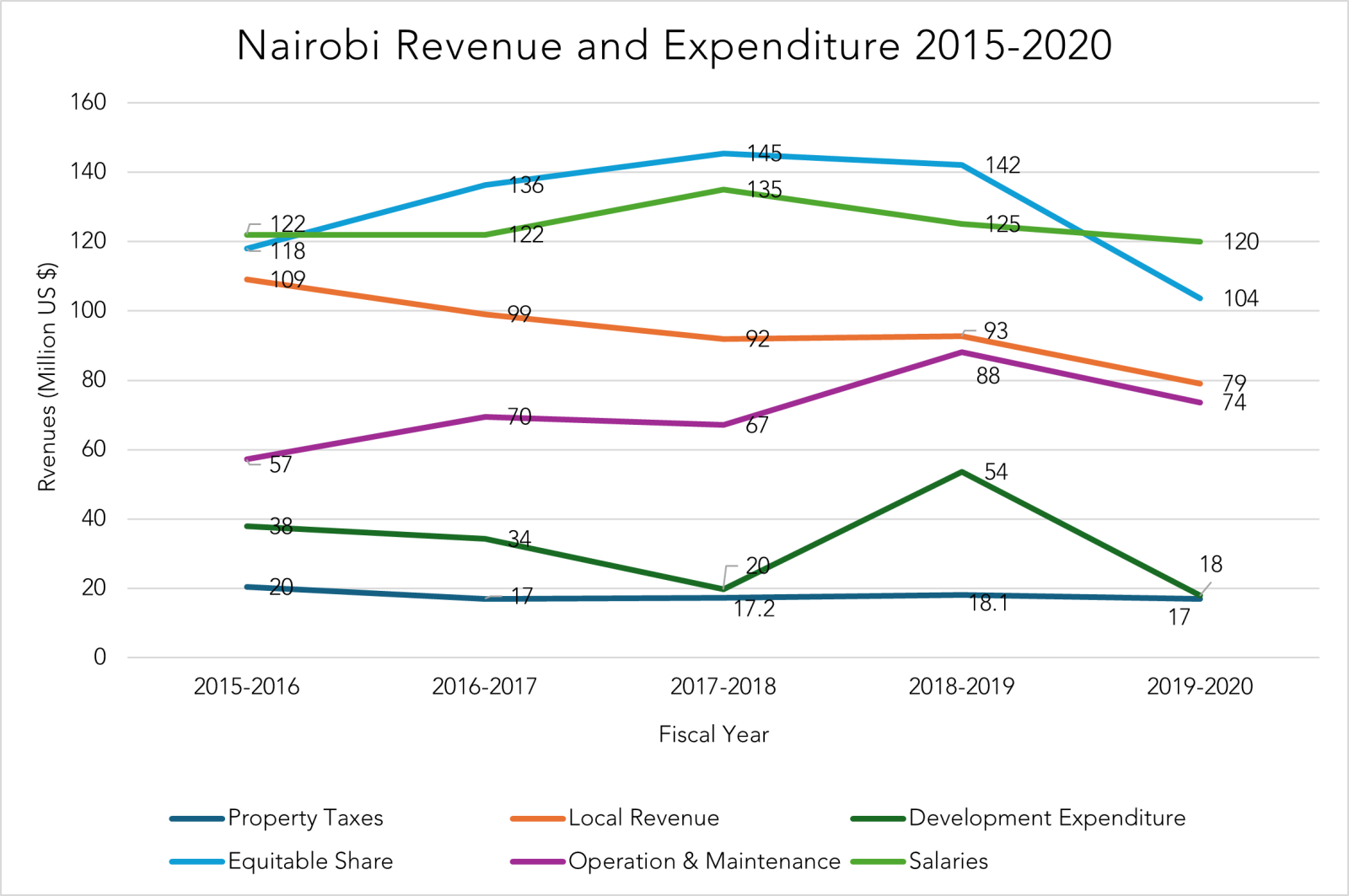

Furthermore, the insistence on using property tax revenues exclusively for development projects overlooks the reality that much of the local government revenue in lower-income countries goes toward salaries and operating expenses for core city governance. From 2015 to 2020 (Charts 1 and 2), property tax revenues in Nairobi averaged US $17.8 million annually, about 18% of locally raised revenues. Development expenditures were nearly double property tax revenues, averaging 32.8% of locally generated revenues. Local revenues raised by Nairobi City – US $ 94.4 million per year – constituted less than 50% of the total budget, with the remainder coming from central government transfers. Salaries alone – US $ 122.4 million annually – exceeded the total locally raised revenue. Although this may reflect poor use of public funds, it demonstrates that only a portion of revenues go directly to development projects.

Key Lessons from Nairobi’s Experience

First, maximizing local accountability without undermining equity requires striking a balance. Empowering local communities to oversee revenue and expenditure and use can strengthen accountability through greater transparency, earmarking, local participatory budgeting, or direct local control over some funds. However, such systems must be designed to ensure development funds are distributed equitably and not disproportionately controlled by the wealthiest.

Second, linking property tax revenues to service delivery is a delicate process. In Nairobi, a significant portion of local revenues goes toward operating costs and salaries. It is reasonable to expect property taxes to contribute to these common costs, as the quality of broader city governance is crucial for all property owners. Service delivery can be enhanced by increasing revenue mobilization and reducing waste, leaving a larger share of funds for development projects and service delivery. Many cities have or are considering, earmarking a portion of revenues for services to encourage efficiency or using government transfers to cover core costs while dedicating a larger share of their own-source revenues to services.

Finally, budgetary transparency and open dialogue can help convey local governments’ efforts to strengthen service delivery alongside the legitimate resource constraints they face, building public trust.

Acknowledgement: The author would like to extend special thanks to Wilson Prichard for his invaluable contributions to the reflections in this blog. Gratitude is also extended to Regan McCort, Priyanka Shah, and Moyo Arewa for their insightful input in refining the draft.

Photo credit to Flickr/Ninara