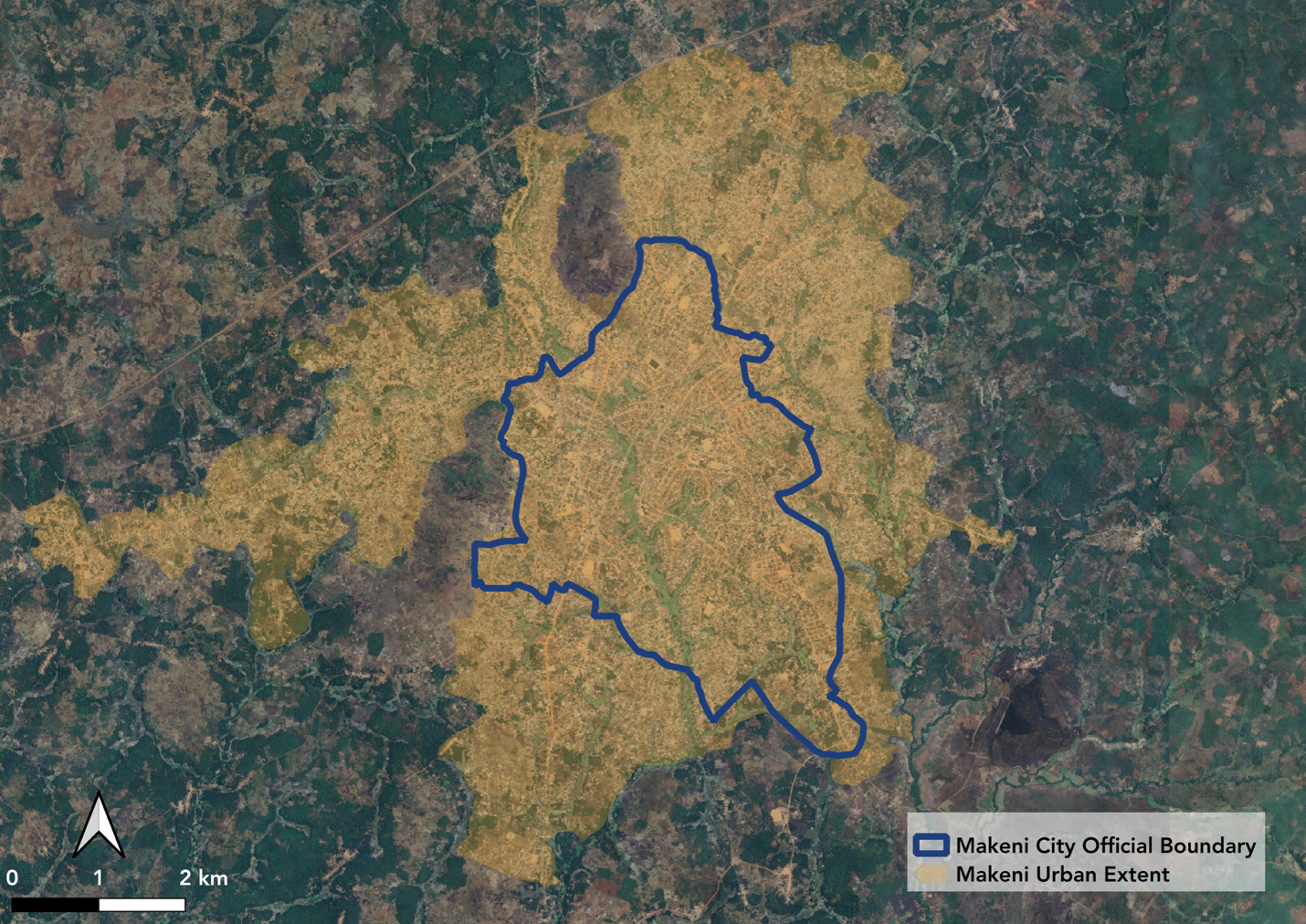

Look at a satellite image of Makeni in Sierra Leone and you will struggle to find the city boundary. The built environment extends continuously along the main arterial roads, with no visible break between the taxable city and the surrounding urban area. Yet for the purpose of funding local services with property taxes, that invisible line determines everything.

This pattern is not unique to Makeni. Across rapidly growing cities in sub-Saharan Africa, built-up areas often extend beyond formal boundaries, especially when those boundaries were drawn to administer elections rather than to reflect urban and economic development on the ground. When adjoining jurisdictions administer markedly different property tax systems, these boundaries raise important questions of equity, and about who should fund local service provision.

Makeni’s Property Tax Reform and the Boundary Problem

Makeni, one of Sierra Leone’s rapidly growing secondary cities, has been the site of a major property tax reform since 2025 supported by the Local Government Revenue Initiative (LoGRI). Unusually, the reform did not stop at the official city boundary. Data collection and assessment covered Makeni’s full urban extent, generating comparable property-level datasets for both the taxable city and the surrounding urban area.

Makeni’s official boundary was drawn from enumeration areas established for the 2015 census and later used for the 2018 elections. By 2025, it covered about 15,600 taxable properties—roughly half the full urban extent of Makeni. Properties inside the boundary are subject to the reformed tax system, while those outside remain under Bombali District Council (BDC) jurisdiction.

With BDC’s cooperation, the reform identified and assessed properties across the full urban extent. But the outside-boundary portion of this data is not currently used to issue tax bills. BDC continues to operate an older, unreformed property tax system. Survey evidence from the area suggests that only about one-in-five properties under BDC jurisdiction receive a tax bill, far below the near-complete coverage within the Makeni City boundary.

In practice, MCC is the local service provider for the wider built-up area, regardless of where the formal boundary falls. Properties outside the boundary draw on the same municipal services and contribute to the same pressures around waste, sanitation, markets, and urban planning.

The result is a structural gap between fiscal authority and de facto service delivery responsibility. Makeni’s property tax data allows us to quantify one dimension of that gap: the revenue MCC could reasonably collect if its fiscal authority extended across the full urban area.

What the Data Shows

Makeni’s official boundary divides a single urban area into two property bases that are, by almost every measure, alike. The reform data covers 15,232 assessable non-government properties inside the boundary and 15,407 outside.1 Outside properties are slightly more domestically concentrated, at 92% compared to 89% inside, but the broader distribution of property types is similar.

Properties inside Makeni’s official boundary have a total revenue potential of NLe 2.85 million (US$127,0002). Properties outside the boundary have a revenue potential of NLe 2.60 million (US$116,000), reflecting a slightly lower concentration of high-value commercial properties. The outside-boundary property base therefore has nearly the same revenue potential as the taxable city itself.

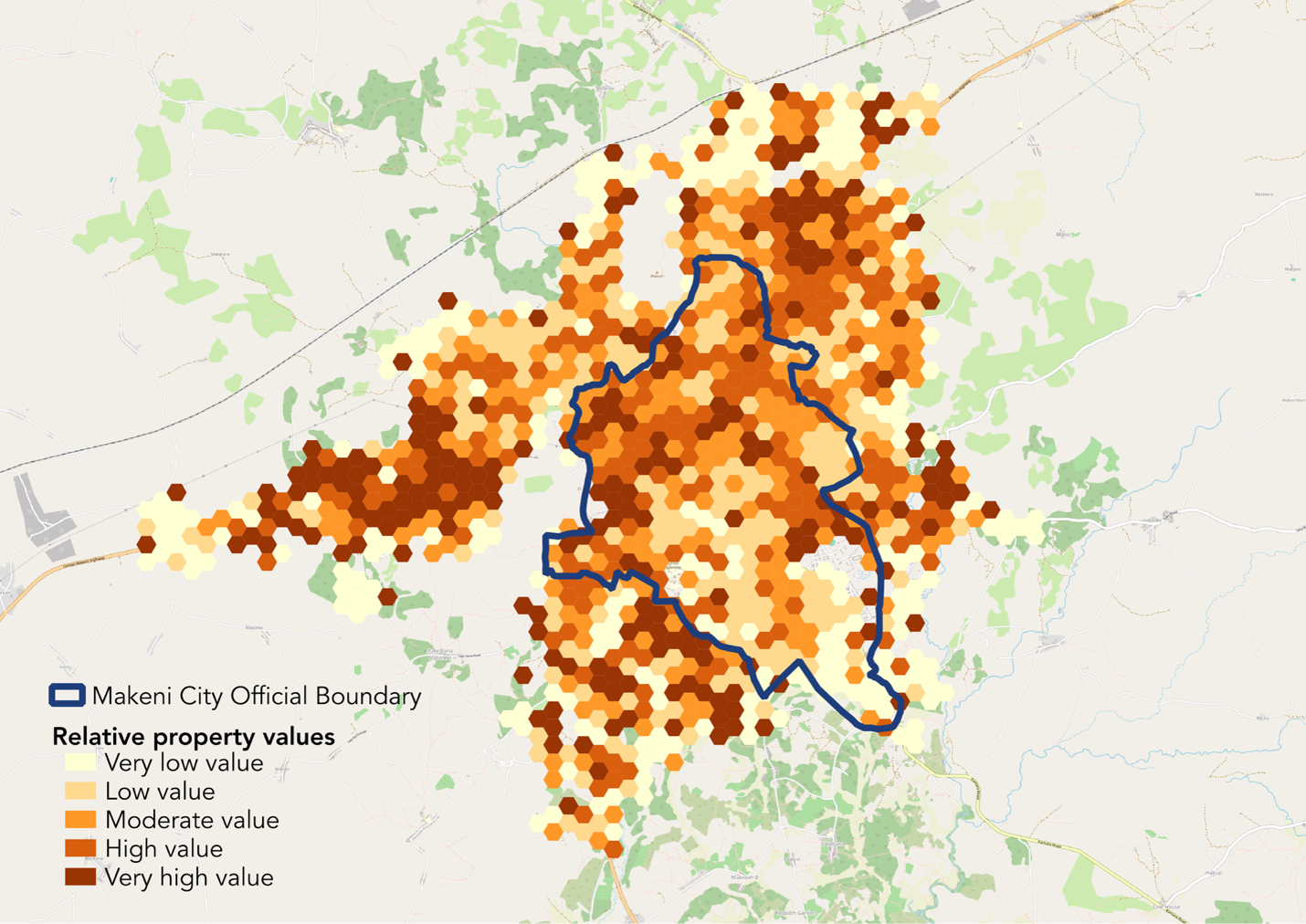

Notably, the distribution of property values across Makeni’s full urban area does not respect the official boundary.

In the map above, each hexagonal cell is coloured by the mean value quintile of properties within it. The official Makeni City boundary is overlaid in blue. Higher-value properties cluster along major road corridors on both sides of the boundary, with no visible break in property values. The boundary therefore does not separate a higher-value urban core from a lower-value rural periphery but rather cuts through a continuous urban property market.

In 2025, MCC collected about NLe 418,000 (US$18,600) from properties inside the boundary. BDC’s most recent reported property tax revenue (from 2022) was just NLe 96,000 across its entire jurisdiction—less than a quarter of what MCC now collects from a much smaller area. Outside boundary properties therefore contribute very little in property tax revenue, through any channel, despite sitting within Makeni’s functional urban area.

This fiscal gap is created by the jurisdictional divide, rather than by any obvious difference in property value, urban form, or administrative visibility. Collections on both sides of the boundary remain low, which helps explain why the gap has attracted relatively little attention. But as compliance improves and property values increase, the revenue at stake will grow substantially, making the gap harder to ignore.

Foregone Urban Sprawl Revenue

Given that the property base outside Makeni’s official boundary is structurally similar to that inside, how much revenue would outside-boundary properties realistically contribute if they were billed by MCC?

To estimate that figure, inside-boundary collection rates can be applied to outside-boundary properties by value quintile. The value distribution of properties on either side of the boundary is nearly identical, making these rates a defensible basis for revenue projection.

| Quintile | AAV range (NLe) | Collection rate |

| Q1 (lowest) | 129 – 2,894 | 12.5% |

| Q2 | 2,894 – 4,474 | 13.0% |

| Q3 | 4,474 – 6,618 | 15.4% |

| Q4 | 6,618 – 10,238 | 15.9% |

| Q5 (highest) | 10,238 – 3,786,421 | 14.6% |

Collection rates rise modestly from the lowest to the fourth value quintile, before dipping slightly in the highest quintile. Applying these compliance rates to the outside-boundary revenue potential of NLe 2,599,180 suggests collections of about NLe 381,000 – an increase of more than 90% over current non-government property tax collections.

Fiscal Authority and Service Delivery Responsibility

Makeni’s reform shows how property tax improvements can expose a deeper governance issue: fiscal authority often stops at boundaries that no longer match the urban areas requiring services. In Makeni, MCC has built a functioning property tax system while the surrounding rural district continues to administer a much weaker one, raising questions of equity and long-term revenue sustainability.

Properties of similar value on either side of the boundary face entirely different tax treatment simply because of where an administrative line falls. Inequity is not just an abstract concern, because perceived unfairness undermines compliance. If taxpayers inside the boundary continue to see similar neighbouring properties contributing little to service delivery, the tax system will look less legitimate and become harder to enforce.

Property taxation works best when there is a visible link between what people pay and the services they receive. That link is weakened when the authority responsible for urban service provision cannot collect revenue from the full area it effectively serves. In Makeni, aligning fiscal authority with the city’s economic and urban reality is therefore not only a revenue issue. It also provides a firmer foundation for more effective local governance.

Wider Lessons from Makeni

The Makeni case is unusually well-evidenced and can provide insight for other cities in the region. It challenges the assumption that urban sprawl properties are lower value than those in the city core. Reform data shows the opposite: the highest-value properties follow the main road corridors outwards, placing many of the areas that would most naturally fund urban services outside the city’s tax base.

The technical work needed to tax Makeni’s full urban extent is already complete. Properties have been identified, assessed, and are included in the tax administration platform. The remaining barrier to revenue collection is jurisdictional, rather than technical or administrative. Reform itself presents an opportunity to clarify urban boundaries early, before the levels of revenue involved become much larger and such changes become more contentious.

At least two broad options follow from the Makeni case. One is formal boundary expansion, which could be implemented gradually by prioritizing the highest-value peripheral areas first. The limitation of this approach is that fast-growing cities may quickly outpace their newly revised boundaries. A second option is to introduce greater legislative flexibility, allowing city councils to tax within their functional urban extent, potentially alongside revenue-sharing arrangements with surrounding district councils.

As more cities in sub-Saharan Africa invest in property tax reform, they are likely to encounter similar jurisdictional challenges. Improved property tax data will reveal not only what cities can collect, but also where fiscal authority no longer matches urban reality. The question of who should pay for the city – and which level of government should collect those payments – will become harder to avoid.

- Government properties are excluded throughout because in practice central government property tax payments in Makeni appear to function more like a negotiated lump-sum intergovernmental transfer, making them a poor basis for projecting compliance behaviour across the boundary. ↩︎

- Using the 2025 average FX rate US$1 = NLe 22.5 ↩︎

Acknowledgements: The author thanks Evan Trowbridge, Robin Benabid Jegaden, Zoé Baudoin, Kevin Grieco, and Wilson Prichard for data inputs, verification of the calculations and arguments, and comments on earlier drafts.